- Lumida Ledger

- Posts

- Buffett is Making Mistakes, Google’s new TPU Chip, Amazon CEO Letter

Buffett is Making Mistakes, Google’s new TPU Chip, Amazon CEO Letter

Ram Ahluwalia

April 14, 2024

Welcome back to the Lumida Ledger.

If you find this valuable, we’d greatly appreciate you sharing it far & wide with your network. That’s how we grow and keep the content free to read.Here’s a preview of what we cover this week:

Macro: Geopolitical Risk

Markets: Homebuilders, Israel vs. Iran tension

Company Earnings: Bank Earnings, JPM Buyback

AI: Google vs. Amazon

If you’re interested in learning more about Lumida’s wealth management services, click to explore becoming a client

GDP is up. The job market is strong, yet the delinquency rates on loans are nearing the Great Financial Crisis levels.

We investigate this paradox this week with William Black, credit expert and previously MD at Moody’s structured consumer finance.

We discuss the health of the US consumer. We also debate China dumping. Is this a subsidy for US consumers, or does it threaten US strategic interests?

Tune in below, and don’t forget to subscribe. It helps us get amazing guests and keeps our content free.

We are back with Lumida Legacy after a short break.

In this episode we explore the power of legacy documentaries with filmmaker Erikson Dickens. Erikson describes his process of turning family stories into generational heirlooms.

Macro

Geopolitical Risk

Stocks were risk-off this past week on concerns of Iran and Israel escalation.

First off, note that conflicts in the Middle East have taken place many times over the last several decades.

Stocks have continued to go higher.

Tactically, however, there are a few considerations.

If there is no escalation, then the entry points we are seeing are attractive. YTD there have not been many good ‘buy the dip’ opportunities.

We see that now. The dip will dip more if geopolitical risk increases.

The US appears to be taking action to quell the risk of an escalation by sending destroyers to the region.

Supposing there is an escalation? What then?

Well, we would be in a risk-off world for about a month give or take.

This is what we saw post 9/11. We also saw this more recently in our analysis of Israel’s stock market after the atrocities of October 7th.

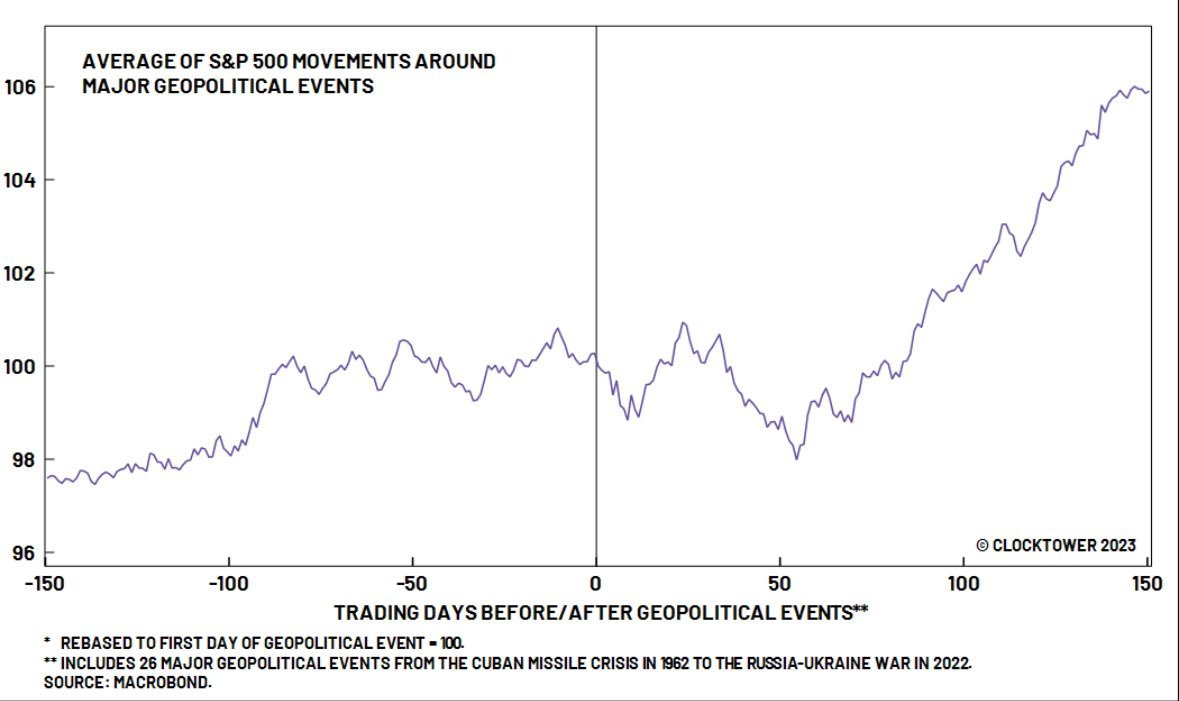

Our friend Stephen McBride from RiskHedge posted this chart:

Notice there is about 2 weeks of sell-off after a geopolitical event.

By trading day number 50 (e.g., 10 weeks) market statistically bottom.

So, if there is an escalation, and a correction ensues - then markets would bottom around Memorial day give or take.

A good approach here is to take a mixed strategy. Deploy some capital now to benefit from this one-off pull back. If markets rally, you have a nice set of entries.

If markets correct due to an escalation, you have some dry powder and can wait. We’ll call out what we think is the next best entry should that happen.

Here is a chart of Israel’s stock market (ticker: EIS). Notice how EIS sold off despite US markets rallying. This index is now a ‘market tell’ for the foreseeable future.

Oil prices are also a market tell:

Oil is approaching YTD highs. Not surprisingly, energy names are benefiting.

If you’re interested in learning more about Lumida’s wealth management services, click to explore becoming a client

Housing Shortage & Mortgage Rates

Per the Kobeissi Letter, “US mortgage demand in March fell to its lowest since 1995, according to Reventure.

Mortgage demand is now 43% below its recent peak and ~16% below the post-2008 lows.

Meanwhile, the average payment on a new mortgage is now nearly $2,800/month.

This means that the average American household would spend ~45% of their PRE-TAX income on a new mortgage payment.

On a post-tax basis, it's over 60% and this doesn't even include taxes, insurance, and maintenance.”

If rates are higher for longer, and there are not enough homes to go around, what needs to be done?

New home construction. Homebuilders have been on a tear despite higher mortgage rates. Take a look.

They also have relatively attractive valuations.

Don’t fall in love with tech - make sure you have exposure to energy and homebuilders.

These two categories, the same categories Buffett has been buying the last few quarters, have secular legs.

The entry for homebuilders is attractive from a short-term perspective.

Our favorite hombuilder is M/I Homes (Ticker: MHO)

The homebuilder focuses on building affordable housing to prime borrowers with an average down payment of 18%.

We like that profile and target customer.

The valuation is cheap at 7.2x. The stock generated ~$550 of cashflow on a $3.2 Bn market cap. The stock has a mix of traits we like: a good valuation, momentum, and a business linked to a secular trend.

The stock is much cheaper than better known homebuilders such as DH Horton or Lennar which are ~30% more expensive.

The stock is under-covered - only 1 analyst covers it. So it will have more volatility than other homebuilders.

At the same time, the stock should benefit from multiple expansion as more analysts cover the name.

MI homes has exposure to Florida, Texas, and North Carolina. Those are markets experiencing population growth and have favorable demographic trends. (The firm also has exposure to other markets such as Ohio.)

Here’s an excerpt from their most recent earnings call:

“Strength of our communities and product offerings, along with our selective and very targeted use of below-market financing incentives contributed to our strong fourth quarter and full year sales performance. In the fourth quarter, we sold 1,588 homes, a 61% increase over last year with significantly better per community absorptions. Clearly, as rates begin to fall in the fourth quarter, we saw a pickup in both traffic and demand. Notably, our December sales were the best month of the fourth quarter. For the full year, we sold 7,977 homes, an increase of 20% over 2022.

Our monthly sales pace during the year averaged 3.3 homes per community compared to a sales pace of 3.1 homes per community during 2022.”

We like the target demographic and the ability to offer financing during a period of higher mortgage rates.

Management also notes that costs have stabilized (we speculate that’s likely due to greater pool of labor from immigration).

The firm ended the the year with $733 million of cash and zero borrowings under its $650 million unsecured revolving credit facility. This

They firm has a considerable amount of undeveloped land. Land is a high beta exposure. They have a 3-year supply of land to develop.

The bear case for MHO is their pipeline - their backlog of homes they have under contract to sell - is shrinking. Some of that is seasonal. Fundamentally, however, these are transient factors.

So, this is a stock that we expect will do well when they report earnings. As the stock gains a following and analyst coverage (which can take 1 to 2 years), we expect the valuation discount versus its peer group will close.

If you’re interested in learning more about Lumida’s wealth management services, click to explore becoming a client

Immigration & Macro

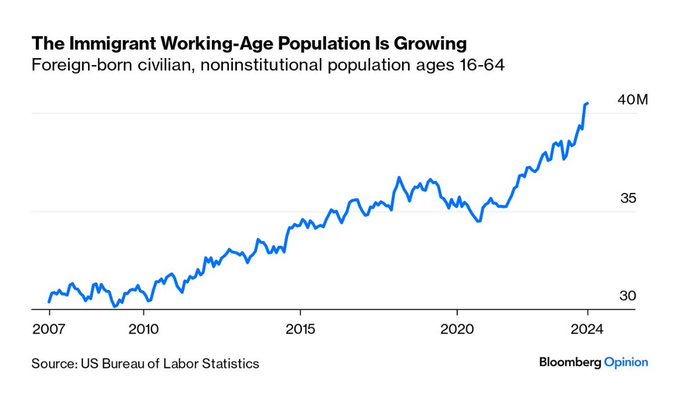

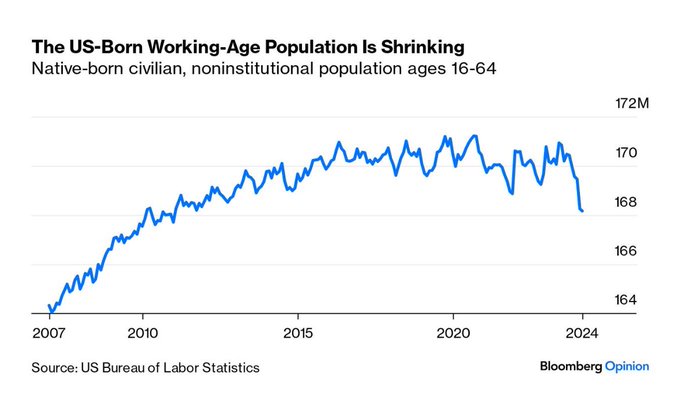

Illegal immigration is one of the key themes we are tracking.

One effect is that immigration is increasing the US working-age population.

That will stave off recession risks (not that we see any signs of recession).

Recessions are in part caused by labor shortages. We saw this in the DotCom era. When there is no one left to higher, wages start to increase, the Fed steps on the brakes and the party is over.

“.. Without immigration, the US working-age population would be shrinking, and this seems likely to remain the case for the rest of the decade. Immigrants are taking all the jobs because, on net, no one else is available.”

The reason why this matters? The US working age population is shrinking.

We’d much prefer a rational legal immigration policy of course. But, we have to play the hand we see in front of us.

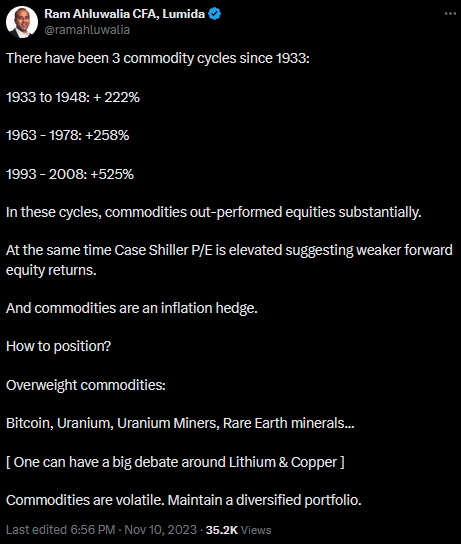

Commodity Cycle

Gold is cranking higher.

But so is Cocoa, Oil, Bitcoin, Copper, and Uranium.

What’s the common theme? Commodities.

The advantage of cross-asset class investing is you can zoom out and see the theme.

The backdrop story is inflation / dollar weakening.

Since the last FOMC meeting, inflation sensitive names like energy are assuming leadership.

Long duration assets like tech have under-performed. Tech hasn’t really gone anywhere in 2 months.

We’re in a commodity cycle.

This is a post we shared in November highlighting the average length and upside from exposure to commodity cycles.

We are betting on the commodity cycle via digital assets and Uranium.

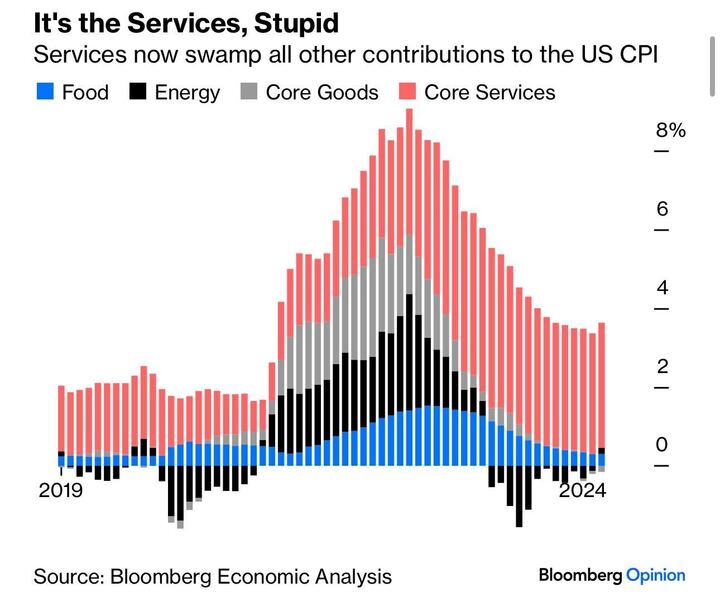

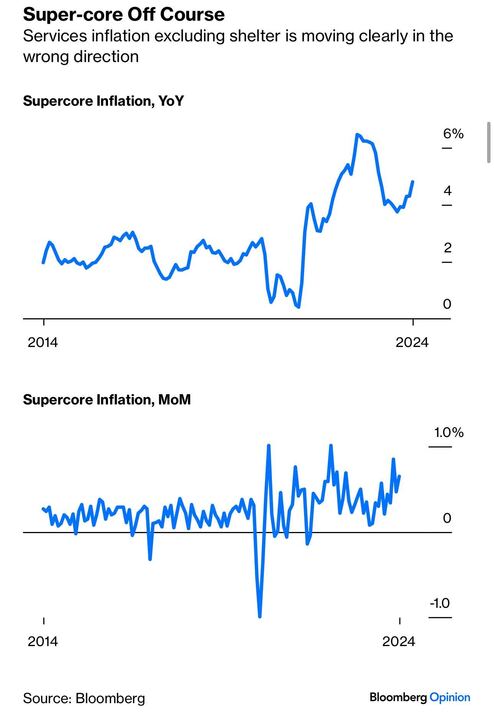

Hot CPI Print

Our Aging Demographics thesis showing up in the CPI report

Home health care for the elderly is up 14%

This is the most challenging and creatively demanding of our investment themes

With our nuclear renaissance thesis, you can simply buy uranium and uranium miners and you are participating. Straightforward.

But, investing against the fastest growing demographic the ‘oldest of the oldest’ has quite a few side quests.

There are so many angles - elderly care, pharmacy, healthcare, at-home care, therapeutics.

We are still actively researching this theme and researching what we believe are attractive risk-adjusted return ideas.

One recent move we shared a few weeks ago is Harrow. That idea is up 15 to 20% since our entry.

Simply put, Harrows lets us get ‘long cataracts’ thru one of their FDA fast tracked drugs.

This is a theme people are aware of, but Mr Market has not figured out how to invest against it other than obvious names in healthcare

Vibe Change:

Ever since the last FOMC day, Mr Market has inflation on his mind.

Take a look at this thread where we first saw this new thematic chord.

Back then I said ‘one day does not a trend make’.

Today, however, we have ample data that Mr Market is dancing to a new tune.

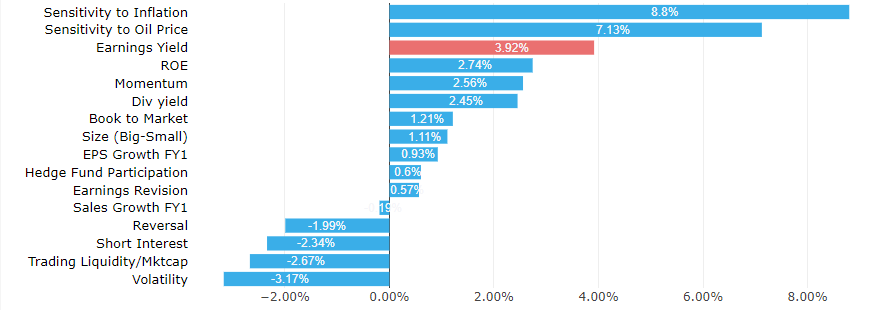

You can see that in the Factor Returns over the last 30 days.

This is saying the following:

Energy stocks are doing well

Stocks negatively correlated to rising rates are hurt (e.g., biotech and small caps)

Buffett type businesses (high ROE, high ROIC, good valuations) are doing well.

Momentum is still working but not longer leading factor as in earlier this year

Hedge fund appetite is waning somewhat

Unprofitable tech and volatility names are getting hurt. That includes the EV sector (e.g., Lucid, Rivian, Tesla, etc.) but also names like Beyond Meat and bitcoin miners.

Adjust accordingly. We have gradually reduced our biotech exposure down. We believe there will be no Fed rate cuts in June. Biotech stocks tend to rally when the Fed starts cutting rates.

We’ll keep stalking this sector to look for good entries sometime over the summer.

We love the biotech theme. The timing is a bit off.

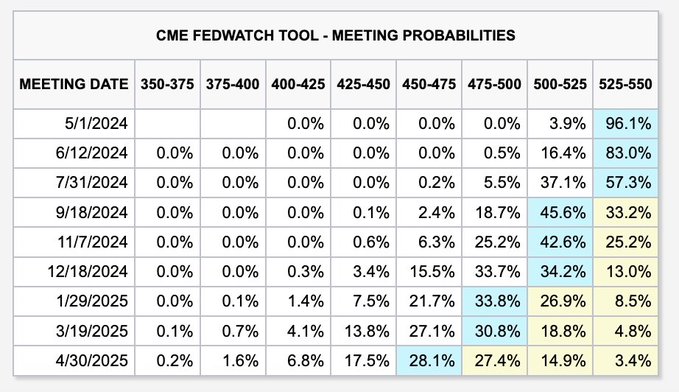

On Fed Rate Cuts

Interest rate futures are now pricing in a 13% chance of ZERO rate cuts this year.

That makes a lot more sense to us. We could see this go higher.

The economy is beating expectations. We have a ‘hot landing’ - hot inflation and a hot economy.

The two go hand-in-hand, in our view. You’d be surprised to hear that is not the conventional wisdom.

So, if there are no rate cuts in June, do we believe there is ample data for rate cuts in July. Doubtful.

In August we have Jackson Hole.

Then September would be the next plausible rate cut. The risk is the Fed would look political if they cut and inflation data has not cooled.

That said, we believe the Fed made the right decision in not cutting rates. We have two Presidential candidates that are pressuring the Fed - most recently in Biden’s prediction for rate cuts and prior to that Trump’s call to re-shape the Fed.

Neither of those calls really help the situation.

The Fed has undoubtedly made serious mistakes over the last ten years. That’s caused the value of the dollar to diminish, and has influenced this commodity super cycle and 2021 valuations of 100x for startups

At least on this call, they got it right.

The base case shows just 2 rate cuts by December with a 57% chance that rates are unchanged THROUGH JULY.

Just 4 months ago, markets were pricing-in 6 to 8 rate cuts in 2024.

5 months ago, Fed Chair Powell made what appeared to be a victory speech and called for 3 rate cuts in 2024.

Now, discussions of another rate HIKE are even back on the table.

Has this Fed made the worst calls of all time?

Futures contracts tied to the federal-funds rate show traders see rates ending the year around 5%, according to FactSet, implying just one or two quarter-point cuts this year. Entering January, traders had expected the Fed to cut interest rates six or seven times.

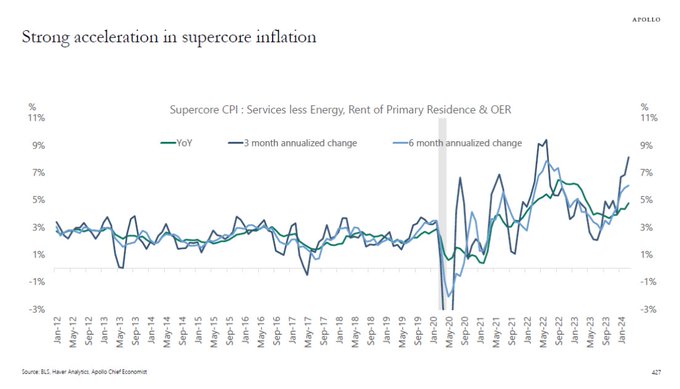

Ryan Wang of HSBC pointed to significant increases in several categories that might be impacted by the tight labor market, such as veterinarian services, funeral expenses and dry cleaning. He said these increases “may tend to reinforce the view of FOMC policymakers who believe that tight labor market conditions represent an upside risk for inflation.”

Per APOLLO: “The number of people going to Broadway shows has been rising faster than normal in recent weeks, likely driven the strong labor market and strong household gains in financial wealth and housing wealth.”

We don’t have enough chips.

We don’t have enough young workers.

We don’t have enough childcare.

We don’t have enough nurses.

We don’t have enough energy.

We don’t have enough uranium.

We don’t have enough biotech / therapeutics.

We don’t have enough housing.

We don’t have enough competition.

We don’t have enough infrastructure.

We don’t have enough datacenters.

We have too much commercial office.

We have too much EV production.

We have too much ESG.

We have too much SAAS.

We have too many processed foods.

We have too much inflation.

We have too much government debt.

We have too much capital allocated in the wrong areas.

How would you translate these statements into an investment portfolio?

Markets

Breakdown of Amazon CEO Andy Jassy's Annual Letter and Thoughts on Amazon

Rough day for tech!

Except for Google which hit all time highs…

On news about their Customer GPU

Which is actually old news and we wrote about it in @LumidaWealth newsletter last year

Google has more semi compute than its competitors combined. And data to match.

Point. Set. Match.

BUFFETT IS MAKING MISTAKES

If you’re interested in learning more about Lumida’s wealth management services, click to explore becoming a client

Let me count the ways…

Here we go:

Buffett sold Taiwan Semiconductor when it had a PE of 15, and kept Apple.

We wrote this in July’s Lumida Ledger:

"The PE ratio for Apple is 32 with a 6% earnings growth expectation. Meanwhile, Taiwan Semiconductor has a PE ratio of 15 and over twice the earnings growth rate expectation of ~10% over the next 5 years”

We were selling Apple last summer as readers know.

(2) Participating in IPOs like Snowflake

I learned to avoid IPOs from Buffett & Munger.

Buffett has a distaste for chasing trends and buying into IPOs or whatever Wall Street is selling.

Snowflake is now below its IPO price and facing slower growth and rising competition.

(Buffett got a better price than the IPO via an off-market deal. Doesn’t change the conclusion.)

(3) Delta Airlines

I learned to avoid airlines from Buffett.

The joke about airlines is ‘you are as smart as your dumbest competitor’.

The high fixed costs and zero marginal cost of operating an airline makes price competition brutal.

Buffett was selling Delta and he marked the bottom in the stock almost to the day when his sales finished.

(4) Apple

Apple was a major win for Buffett and a foray for Berkshire into tech stocks.

But, Apple’s earnings growth went to 0% ish over the summer.

iPhone upgrade cycles are slowing.

Berkshire should have gradually started selling last summer (like we did).

(5) Bank of America was a new position for Berkshire following the 2008 crisis

Buffett has a fondness for banks (see $ALLY, $AXP, $GS, $WFC etc over the years).

$BAC has a significant unrealized hold to maturity loss on its balance sheet.

Buffett missed this.

JPM has outperformed BAC substantially over the last 10 years (15% vs 10% and has a cleaner balance sheet)

(6) Wells Fargo

Wells opened up fake bank accounts.

Congressional testimony ensued and the stock was under pressure.

Buffett started selling.

Now the stock is at an all time high.

Ironically, Buffett’s first position in American Express was established after the stock was dislocated due to negative headlines.

(7) Investing in Tech

Buffett is displaying ‘style drift’

He invested in HP, Sirius, IBM, electric auto firm $BYD

(8) 2023 Mini Crisis

Buffett provided rescue capital and scooped up interests in several banks in 2008.

He did not pull the trigger in 2024.

(We scooped up JPM and UBS at the time. Here are the receipts for newer readers.)

Banks are in Buffett’s wheelhouse.

Why did he not swing?

(8) What is Berkshire doing well?

Buffett will do well on energy firm Occidental Petroleum.

That’s classic Buffett. He’s accumulating $OXY on dips.

I don’t own it (preferring energy services firms with lower valuations), but for his size that makes sense.

Buffett is also scooping up homebuilders.

This should do well.

We have a massive housing shortage.

That trend is intact.

Company Earnings

Banking:

Major banks like JPMorgan Chase and Wells Fargo reported solid revenue and earnings growth, driven by improvement in net interest income and trading/investment banking performance

JP Morgan sold off on comments in analyst Q&A from Dimon suggesting that the stock was over-valued in the context of the firm’s $2 Bn buyback per quarter program

The funny thing… This will actually improve shareholder ROE if JP Morgan buys the dip on its own stock!

Asset manager BlackRock saw assets under management (AUM) reached new highs, aided by strong long-term net inflows

Citigroup also beat expectations, with investment banking revenues jumping 35% amid increased debt and equity issuance activity

Consumer:

Beverage company Constellation Brands posted healthy revenue growth, led by robust performance in its beer segment which outpaced the broader U.S. beer market

Industrials:

Delta Airlines reported better-than-expected revenue and earnings, though its capacity (CASM) metrics still face year-over-year pressure despite improvement

AI

Guess how many data centers there are in Saudi. Don’t cheat.

Saudi Arabia has 60 data centers.

That’s one country. Many countries will invest in their own Sovereign AI because they do not trust US based hyperscalers.

Investing in the Datacenter trend is a nice secular idea.

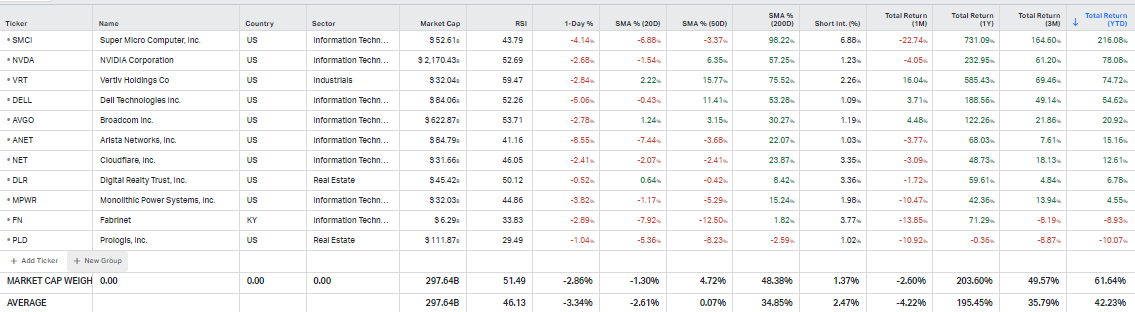

Here is our Datacenter watchlist. We own several names here, but not all. We used to own CloudFlare. We made that call on Twitter. It’s run up quite a bit. We think it’s over-valued and sold it.

We also believe Data Center REITS like Prologis (PLD) and Digital Realty Trust (DLR) are over-valued when you comp them to firms like CoreWeave (we own it!)

Let me know if you think we are missing names that are exposed to the Data center trend.

The Search Engine LLM Wars

Some observations/questions:

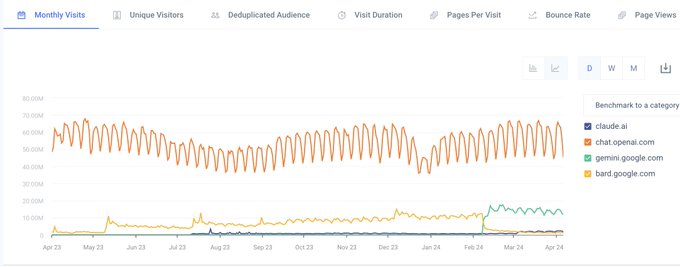

Google Gemini traffic is already ~25% of ChatGPT?

And Google isn't pushing it through their massive distribution channels yet (Android, Google, GSuite, etc).

ChatGPT is still the big brand, but its usage is relatively flat over the last year. That matches my own usage.

Beth Kindig reports that Google unveiled a new data center AI chip, its TPU v5P.

It’s an Arm-based $ARM CPU called Axion.

Axion will be available on Google Cloud, and Google claims it offers 50% better performance compared to current x86 chips from Intel INTC and AMD.

Google is spending far less on CapEx than both Amazon and Microsoft. That’s great for Google’s earnings longer-term.

Jefferies flagged a WSJ about how Google $GOOGL is expanding its in-house chip efforts to reduce reliance on $INTC, $NVDA and other outside chipmakers.

This seems to be talking about the Axion CPUs, which use $ARM circuitry, and should pose limited read-thru for GPUs.

The news reads negatively for INTC and AMD, which sell to hyperscalers like Google, but could be positive for Broadcom and ARM which provide custom chip design solutions.

More from the WSJ: "Google is making more of its own chips, rolling out new hardware that can handle everything from YouTube advertising to big data analysis as the company tries to combat rising artificial-intelligence costs.

The new chip, called Axion, adds to Google’s efforts stretching back more than a decade to develop new computing resources, beginning with specialized chips used for AI work. Google has leaned into that strategy since the late 2022 release of ChatGPT kicked off an arms race that has threatened its dominant position as a gateway to the internet.

The chip efforts promise to reduce Google’s reliance on outside vendors and bring it into competition with longtime partners such as Intel and Nvidia, analysts said. Google officials said they didn’t view it as a competition. “I see this as a basis for growing the size of the pie,” said Amin Vahdat, the Google vice president overseeing the company’s in-house chip operations. Google owed much of its early success to an investment in the chips necessary to fuel the company’s web search algorithm.

That often meant piecing together cheap, commercially available hardware in novel ways. The boom in AI and its need for vastly more computing resources has pushed Google further in the direction of custom solutions. It has credited specialized AI chips it built, known as tensor processing units, or TPUs, with helping save money on services that make heavy use of AI.

Google has worked closely with semiconductor company Broadcom since 2016 to produce bespoke hardware. Broadcom’s custom-chip division had a surge in business after Google rapidly increased production of TPUs recently, Chief Executive Hock Tan said during a March internal presentation.

The increase, he said, was partly in response to Microsoft incorporating AI features into its Bing search engine, going directly after Google’s core business."

Signs of the Apocalypse

Well, we had an eclipse last week. Here’s the evidence that we are seeing signs of the apocalypse. ;)

1. Earthquake in NJ

2. Eclipse

3. Nvidia down 1%

4. Cannot share $NFLX password to watch Three Body Problem

5. The impossible happens.

A memecoin is listed on public markets: $DJT coin lists under the watch of the SEC.

6. Wall Street Bets goes public $RDDT

There you have it.

Meme of the Week:

Click below to see

Quote of the Week

“What a company's been earning doesn't mean anything. What you have to look at is what people think it's going to earn. If you can see something in two years is going to be entirely different than the conventional wisdom, that's how you make money.”

Stanley Druckenmiller

If you enjoy the Lumida Ledger, please forward share with a friend or subscribe.

If you’re interested in learning more about Lumida’s wealth management services, please join our waitlist.

Disclaimer: Lumida Wealth Management LLC (‘Lumida”) is located in New York, NY, and is an SEC registered investment adviser. SEC registration does not constitute an endorsement of the firm by the Commission nor does it indicate that the adviser has attained a particular level of skill or ability. Lumida only transact business in those states in which it is registered, or qualifies for an exemption or exclusion from registration requirements. Any direct communication by Lumida with a prospective client will be conducted by a representative that is either registered or qualifies for an exemption or exclusion from registration in the state where the prospective client resides.

The information in this material has been obtained from sources believed to be reliable. While all reasonable care has been taken to ensure that the facts stated in this material are accurate and that the forecasts, opinions and expectations contained herein are fair and reasonable, Lumida, Inc. and Lumida Wealth Management LLC (collectively Lumida) make no representations or warranties whatsoever the completeness or accuracy of the material provided, except with respect to any disclosures relative to Lumida. Accordingly, no reliance should be placed on the accuracy, fairness or completeness of the information contained in this material. Any data discrepancies in this material could be the result of different calculations and/or adjustments. Lumida accepts no liability whatsoever for any loss arising from any use of this material or its contents, and neither Lumida nor any of its respective directors, officers or employees, shall be in any way responsible for the contents hereof, apart from the liabilities and responsibilities that may be imposed on them by the relevant regulatory authority in the jurisdiction in question, or the regulatory regime thereunder. Opinions,forecasts or projections contained in this material represent Lumida’s current opinions or judgment as of the day of the material only and are therefore subject to change without notice. Periodic updates may be provided on companies/industries based on company-specific developments or announcements, market conditions or any other publicly available information. There can be no assurance that future results or events will be consistent with any such opinions, forecasts or projections, which represent only one possible outcome. Furthermore, such opinions, forecasts or projections are subject to certain risks, uncertainties and assumptions that have not been verified, and future actual results or events could differ materially. The value of, or income from, any investments referred to in this material may fluctuate and/or be affected by changes in exchange rates. All pricing is indicative as of the close of market for the securities discussed, unless otherwise stated. Past performance is not indicative of future results. Accordingly, investors may receive back less than originally invested. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The opinions and recommendations herein do not take into account individual client circumstances, objectives, or needs and are not intended as recommendations of particular securities, financial instruments or strategies to particular clients. The recipients of this material must make their own independent decisions regarding any securities or financial instruments mentioned herein and should seek advice from such independent financial, legal, tax or other adviser as they deem necessary. Lumida may trade as a principal on the basis of its views and research, and it may also engage in transactions for its own account or for its clients’ accounts in a manner inconsistent with the views taken in this material, and Lumida is under no obligation to ensure that such other communication is brought to the attention of any recipient of this material. Others within Lumida may take views that are inconsistent with those taken in this material. Employees of Lumida not involved in the preparation of this material may have investments in the financial instruments or securities (or derivatives of such financial instruments or securities) mentioned in this material and may trade them in ways different from those discussed in this material. This material is not an advertisement for or marketing of any issuer, its products or services, or its securities in any jurisdiction.